Many Ford owners believe that choosing Premium Care means they are fully protected from unexpected repair costs. The name itself creates a sense of complete coverage, which often leads to a dangerous assumption. The reality is very different. Even the highest tier extended warranty from Ford comes with clear exclusions that can leave drivers facing expensive bills when they least expect it.

This misunderstanding becomes a real problem when a vehicle starts showing signs of wear or damage. Owners walk into a service center expecting coverage, only to discover that the issue falls outside the warranty scope. This situation creates frustration, financial pressure, and a loss of trust in the product.

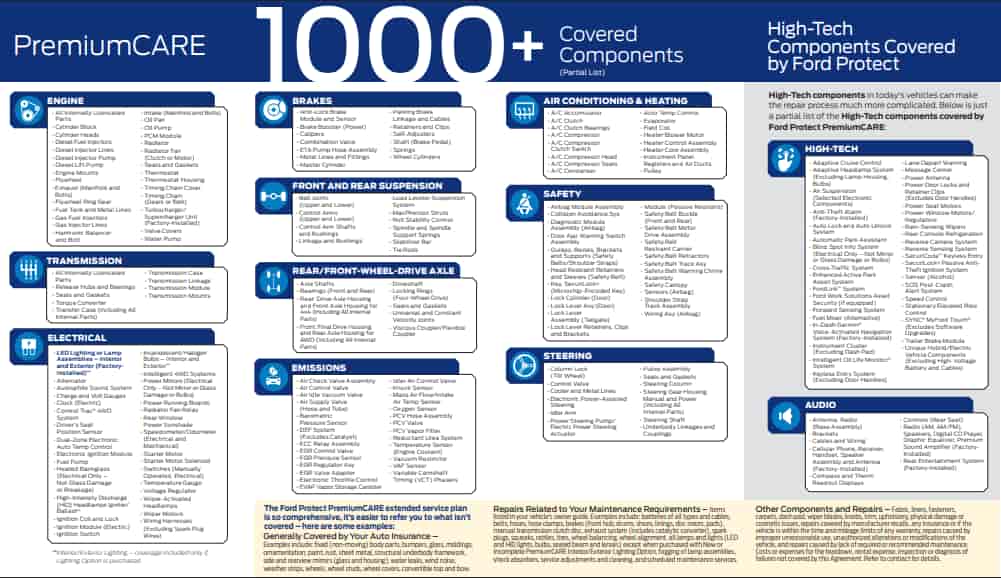

Ford Premium Care is designed to cover mechanical breakdowns, not everything that happens to your car. That distinction is critical. In this guide, you will learn exactly what is not covered under Ford Premium Care, including the most common exclusions and the hidden limitations that many drivers overlook. Understanding these gaps will help you make smarter decisions, avoid claim rejections, and protect your long term vehicle investment.

Contents

Understanding Ford Premium Care Coverage Scope

Ford Premium Care is often described as the most comprehensive extended warranty offered by Ford. It covers hundreds of components across major systems such as the engine, transmission, steering, braking, and electrical systems. However, the key principle behind this plan is very specific. It only applies to mechanical breakdowns caused by defects in materials or workmanship.

This means the warranty is not designed to function as a full protection package for every issue your vehicle may encounter. Instead, it focuses on unexpected failures rather than predictable or gradual deterioration. This distinction is where many misunderstandings begin.

From a technical perspective, Ford separates vehicle issues into two main categories. The first category includes sudden mechanical failures, which are typically covered. The second category includes wear, maintenance, and external damage, which are almost always excluded. Understanding this classification helps you quickly identify whether a repair is likely to be approved or denied.

Another important factor is that extended warranties are structured to reduce risk for the provider. If every type of damage were included, the cost of the plan would increase significantly. As a result, exclusions are not a limitation of Ford alone but a standard practice across the automotive industry.

By understanding how Ford Premium Care defines coverage, you can avoid unrealistic expectations and make better decisions when evaluating repair situations. This knowledge also prepares you to fully understand what is not covered under Ford Premium Care, which is where the most costly surprises usually occur.

What Is Not Covered Under Ford Premium Care

Wear and Tear Items

One of the biggest gaps in Ford Premium Care coverage involves wear and tear components. These are parts that naturally degrade over time through normal use. Because their deterioration is expected, they are not considered mechanical failures.

Common examples include brake pads, tires, wiper blades, and clutch linings. Interior materials such as seat fabric and trim can also fall into this category when damage occurs gradually. Even if these parts fail earlier than expected, they are still classified as consumables rather than warrantable components.

This is where many vehicle owners feel frustrated. Brake systems, for example, are critical for safety, yet replacement costs are not covered. The logic from the manufacturer’s perspective is simple. These parts are designed to wear out, so their replacement is part of regular ownership rather than an unexpected expense.

Understanding this exclusion is essential because wear items represent some of the most frequent maintenance costs over a vehicle’s lifetime.

Routine Maintenance Services

Another major exclusion under Ford Premium Care is routine maintenance. This includes all scheduled services required to keep the vehicle operating properly.

Typical examples are oil changes, filter replacements, tire rotations, wheel alignments, and general inspections. These services are necessary to maintain performance and prevent damage, but they are not covered by the warranty.

This often becomes a hidden pain point for owners who assume that an extended plan will reduce overall ownership costs. In reality, maintenance remains a separate responsibility. Skipping these services can even create bigger problems, as it may lead to denied warranty claims later.

Ford requires owners to follow the recommended maintenance schedule. If a failure occurs and there is evidence of neglected service, the claim can be rejected. This creates a double risk where the repair is not covered and the cost becomes even higher due to compounded damage.

Cosmetic and Interior Damage

Ford Premium Care does not cover cosmetic issues or interior damage unless they are directly caused by a covered mechanical failure. This means that visual imperfections are excluded even if they affect the overall appearance of the vehicle.

Examples include paint scratches, dents, faded surfaces, cracked dashboards, and torn seats. These issues are considered aesthetic rather than functional. As a result, they fall outside the warranty scope.

This exclusion is important for owners who want their vehicle to maintain a like new condition. While Premium Care protects performance related components, it does not help preserve visual quality. Repairs for cosmetic damage can still be costly, especially for modern vehicles with advanced materials and finishes.

Because of this limitation, some drivers choose to purchase separate protection plans or insurance products that specifically cover cosmetic repairs.

Damage from Accidents and External Factors

Ford Premium Care does not cover damage caused by external events. This includes situations that are outside the control of the vehicle’s internal systems. Even though the damage may be severe, it is not classified as a mechanical breakdown.

Typical examples include collisions, fire, flooding, vandalism, and extreme weather conditions. For instance, if your engine fails after a flood, the repair will not be covered under the warranty. Instead, these cases fall under auto insurance policies.

This is one of the most misunderstood areas. Many drivers expect their extended warranty to act as a safety net for all major incidents. However, warranties and insurance serve completely different purposes. A warranty protects against defects, while insurance protects against unpredictable external risks.

Failing to understand this distinction can lead to costly surprises, especially after major incidents where repair bills can reach thousands of dollars.

Misuse, Neglect, or Lack of Maintenance

Another critical exclusion involves how the vehicle is used and maintained. Ford Premium Care requires owners to follow proper usage guidelines and maintenance schedules. If these conditions are not met, coverage can be denied.

Examples of misuse include racing, off road driving beyond recommended limits, or consistently overloading the vehicle. Neglect can involve skipping oil changes, using incorrect fluids, or ignoring warning signs from the vehicle.

This category is particularly important because it can invalidate coverage even for parts that would normally be protected. For example, if an engine fails due to poor maintenance, the repair claim may be rejected entirely.

From a technical standpoint, the warranty assumes that the owner plays a role in preserving the vehicle’s condition. When that responsibility is not fulfilled, the risk shifts back to the owner.

Aftermarket Modifications and Non Ford Parts

Ford Premium Care does not cover failures caused by aftermarket modifications or non approved parts. This includes any alteration that changes the original design or performance of the vehicle.

Common examples include performance upgrades, suspension modifications, third party electronics, and custom tuning. While these upgrades may enhance driving experience, they also introduce variables that the manufacturer cannot control.

If a modified component contributes to a failure, the warranty claim may be denied. In some cases, even unrelated systems can be affected if the modification is deemed to have influenced overall performance.

This creates a significant risk for car enthusiasts. Installing non approved parts may seem harmless at first, but it can lead to unexpected repair costs later. Understanding this limitation helps owners make informed decisions before modifying their vehicle.

Commercial Use Limitations

Ford Premium Care is primarily designed for personal use vehicles. If the vehicle is used for commercial purposes, coverage may be limited or completely voided.

Examples of commercial use include ride sharing services, delivery operations, taxi services, or fleet usage. These activities increase vehicle wear and usage intensity, which raises the likelihood of component failure.

Because of this higher risk, standard warranty plans do not apply in the same way. Vehicles used commercially often require specialized coverage designed for business operations.

This is an important detail that many owners overlook. Using a personal vehicle for income generation without adjusting the warranty plan can result in denied claims when repairs are needed most.

Hidden Limitations Most Owners Overlook

Even when drivers understand what is not covered under Ford Premium Care, many still overlook the finer details hidden in the warranty structure. These limitations are not always obvious, but they can directly affect how much you actually pay when a repair is needed.

One of the most important factors is the deductible. Many plans require a fixed payment for each repair visit. This means even if a component is covered, you still share part of the cost. Over time, multiple repair visits can add up and reduce the perceived value of the warranty.

Another limitation involves coverage duration and mileage caps. Ford Premium Care only applies within a specific time frame or mileage limit, whichever comes first. Once you exceed either threshold, coverage ends immediately. This creates a risk for drivers who accumulate mileage quickly.

Pre existing conditions are also excluded. If a problem existed before the warranty was activated, it will not be covered. This is especially important for used vehicle owners who purchase extended coverage later.

In some cases, diagnostic fees may not be fully covered unless the repair itself is approved. This means you could still pay for inspection even if the claim is denied. These hidden details often create frustration because they are not clearly understood at the time of purchase.

Real Life Scenarios Where Claims Get Denied

Understanding exclusions becomes easier when you look at real situations that happen to vehicle owners. These scenarios highlight how small misunderstandings can lead to expensive outcomes.

A common example involves brake replacement. A driver may notice reduced braking performance and expect coverage under Premium Care. However, since brake pads are classified as wear items, the claim is denied. The owner must pay out of pocket for the replacement.

Another frequent case involves engine damage caused by poor maintenance. If oil changes are skipped or delayed, internal components may wear out prematurely. Even though the engine is normally covered, the claim can be rejected because the failure resulted from neglect rather than a defect.

Flood damage is another scenario that leads to confusion. After driving through heavy rain or flooded roads, water can enter critical systems and cause serious failure. Many drivers assume their warranty will cover the repair, but this type of damage is classified as an external factor and is not included.

These real life examples show that most claim denials are not random. They are directly linked to the exclusions outlined in the warranty. Knowing these situations in advance can help you avoid making costly assumptions.

Conclusion

Understanding what is not covered under Ford Premium Care is just as important as knowing what is included. While this plan offers extensive protection for mechanical breakdowns, it is not an all inclusive solution. Key gaps such as wear and tear items, routine maintenance, cosmetic damage, and external events can still lead to significant out of pocket expenses.

The biggest risk for most vehicle owners is not the cost of the warranty itself, but the false expectation that everything will be covered. This misunderstanding often leads to frustration when claims are denied.

By clearly understanding these exclusions, you can make smarter decisions about vehicle ownership, maintenance, and additional protection options. You will also be better prepared to evaluate whether Ford Premium Care truly fits your needs.

Before purchasing any extended warranty, take the time to review the exclusion list carefully. Ask questions, clarify terms, and align the coverage with your driving habits. A well informed decision today can save you from unexpected financial stress in the future.